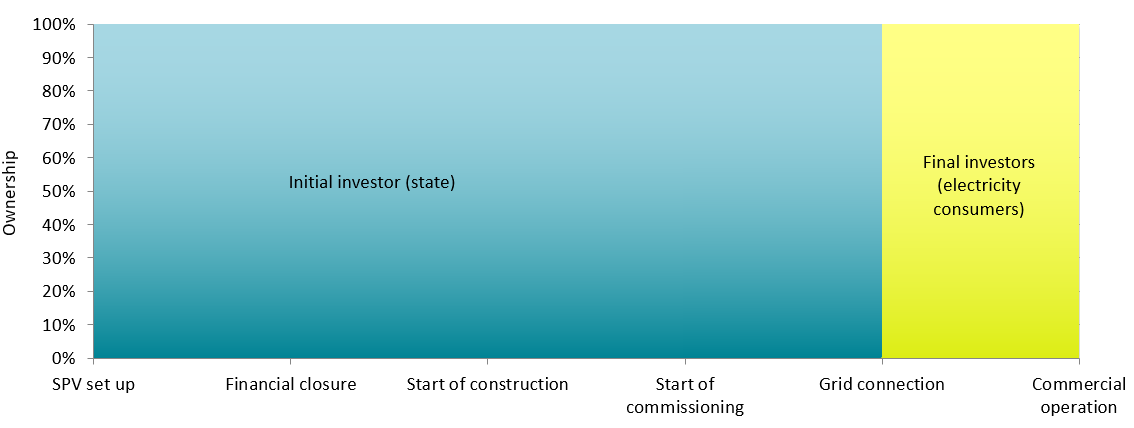

The simplest version of the SaHo Model showing its main assumptions. During the project pre-development, development and subsequent construction phase, the nuclear unit is wholly owned by the state. Once connected to the grid, all shares of the unit are sold to end-users. In practice, this version can be applied to First-Of-A-Kind (FOAK) projects. This may be the first implementation of the SaHo Model in a given country, or the first project in a given technology, when the concerns of potential final investors about the project completion discourage them from buying shares before the construction is completed. In the case of Poland, given the current energy situation, this option would rather apply to SMR technologies, which are FOAK technologies.

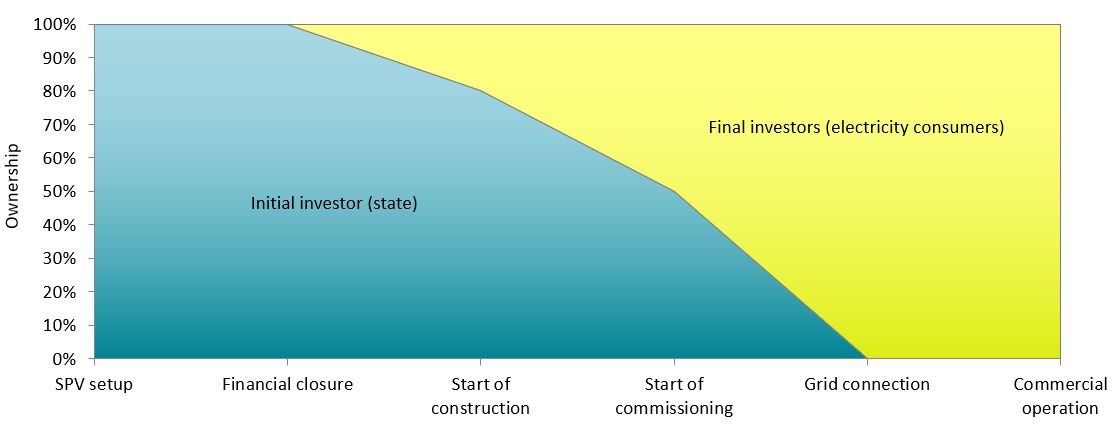

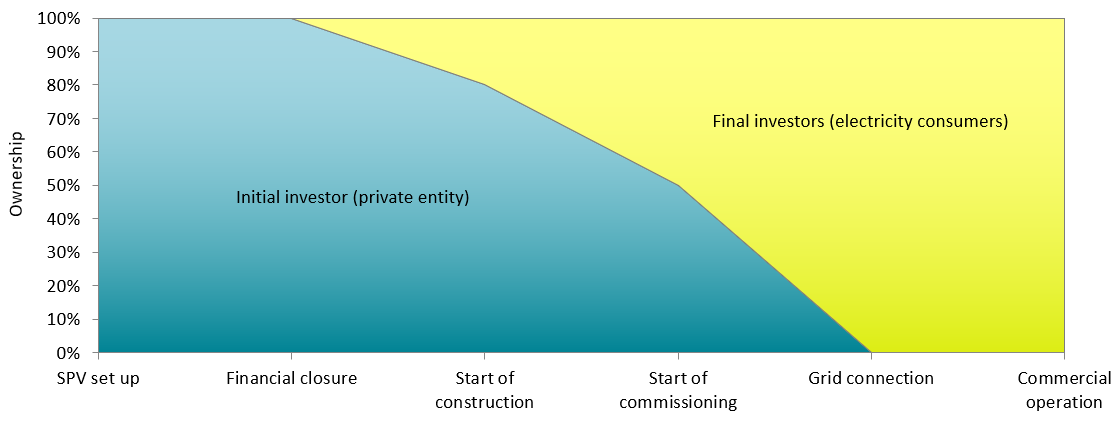

In this version of the SaHo Model the sale of shares begins just after the financial closure and before any significant physical work on site begins. Sale of shares takes place gradually over the entire duration of construction, roughly in proportion to the decline in investment risk, with the last shares going to final investors just before the reactor is connected to the grid.

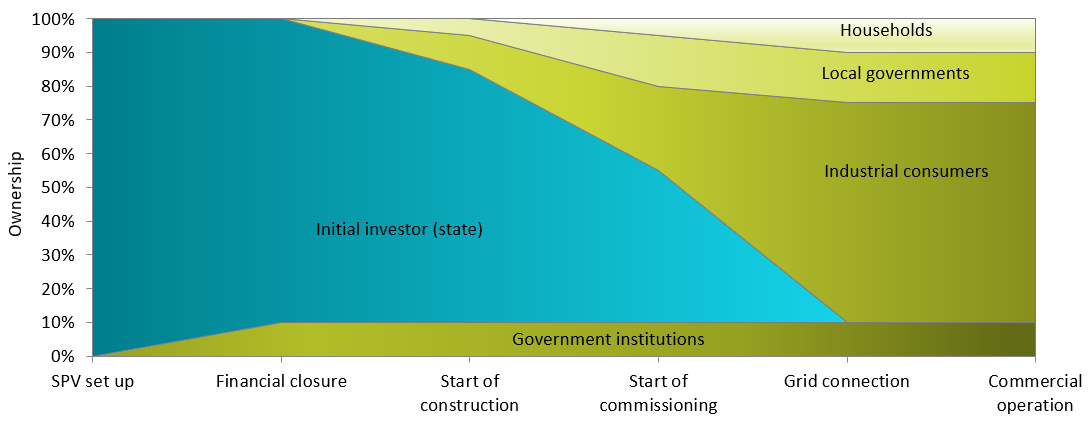

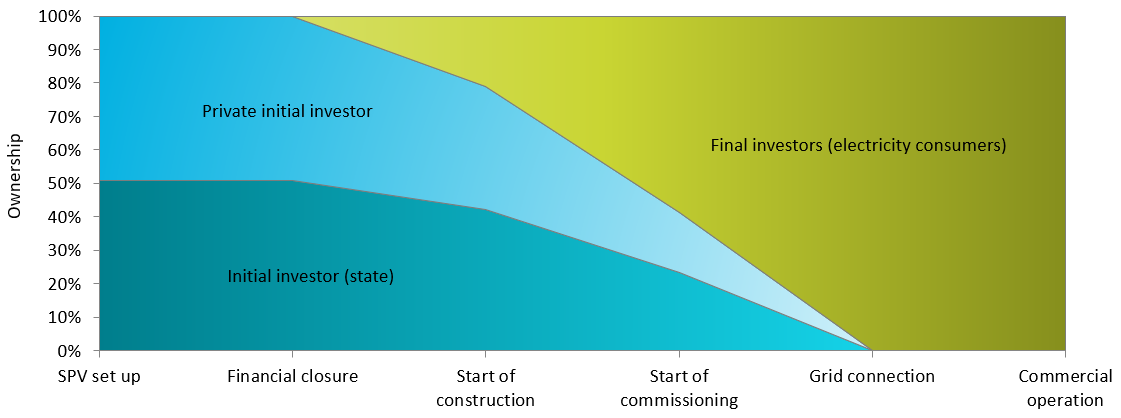

An expanded, more detailed version of the Model with a gradual sale of shares to final investors. This version presents an illustrative ownership structure by selected types of final investors, i.e. government institutions, industry, local governments and households (indirectly through aggregators, e.g. energy cooperatives). The ownership structure is just illustrative but, in the Authors’ opinion, appears to be the most realistic, i.e. the dominant group would probably be industrial consumers or companies from various sectors, not only industry (e.g. transport, logistics, trade).

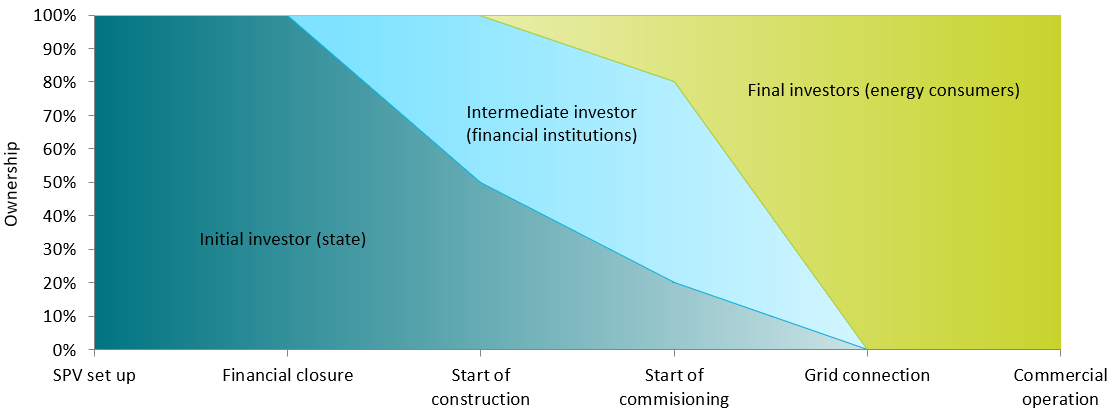

This version emphasises the role of financial institutions. They can play the role of intermediate investor, which buys part of the shares from the primary investor during construction, then takes part of the risk of the investment and subsequently sells the shares to final investors. Such an option can increase the credibility of the project and motivate timely completion of the investment. The sale price of the shares to the final investors will certainly be higher than their purchase price (due to the reduced investment risk), allowing the financial institution to get a correspondingly high rate of return.

This version of the Model was prepared for projects where part of the shares are held by a reactor vendor cooperating with associated energy company and financial institution, who are considered a private primary investor. This group of entities acts as a second primary investor which, like the state primary investor, seeks to sell shares in the nuclear unit to final investors before connecting it to the electricity system.

A version of the Model similar to the basic concept (B), except that instead of the state the project is carried out exclusively by a private entity (or group of entities). Such an entity must meet the following conditions: (a) it is not controlled by the government of the host country, (b) it is able to take the risk of the construction period, (c) it guarantees the completion of the project, (d) it has access to low-cost capital, (e) its goal is to sell shares to final investors before the NPP is operational.

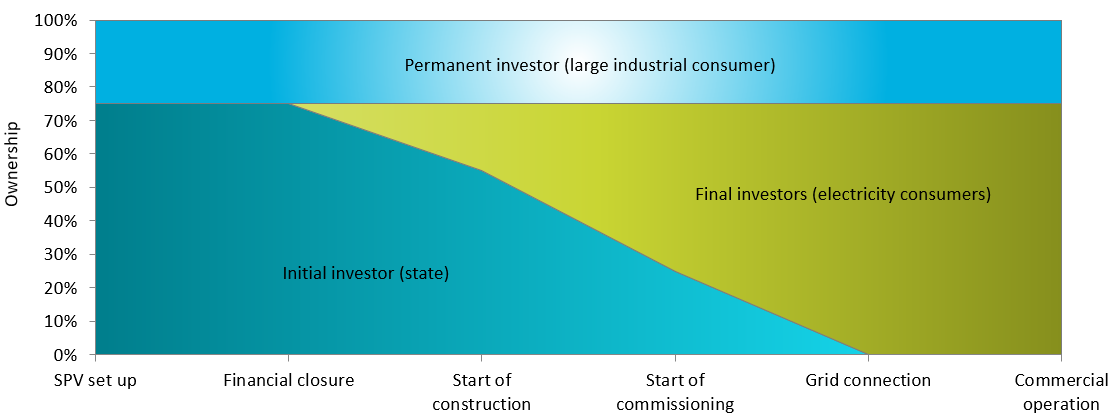

In this version of the Model there is a second investor (called the permanent investor) in addition to the primary investor (state or private). This investor owns a certain number of shares in the nuclear unit from the beginning of the project and maintains this ownership also during the operation phase. Such an investor can be, for example, a large industrial consumer.

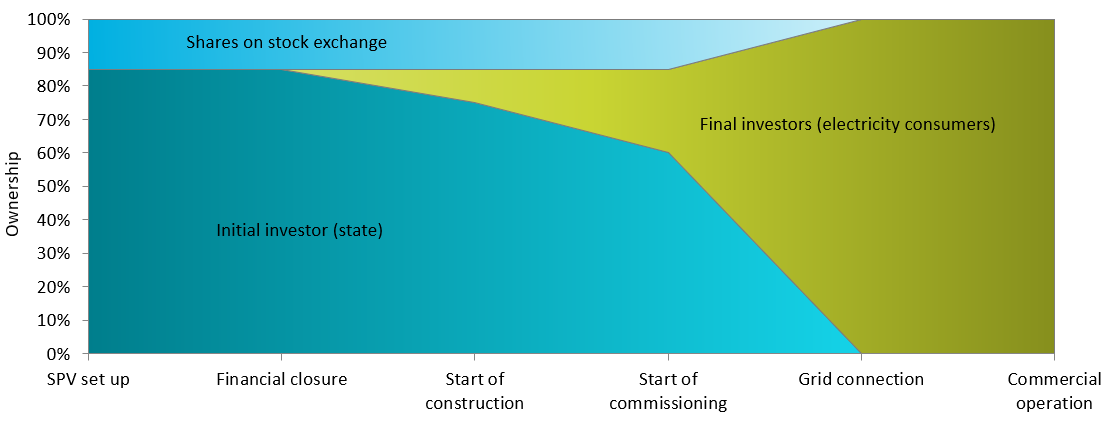

In this version of the Model some portion of the shares is listed on a stock exchange. A certain number of the company’s shares may be offered to investors already at the time of the share issue or later when the initial investor decides to do so. The shares can only be listed on the stock exchange until the power unit is connected to the grid. From this moment the shares can be retained by investors giving them rights to offtake energy in proportion to ownership. They can also be contributed to an aggregator such as an energy cooperative or sold to other final investors.

The advantage of this solution is the possibility to voluntarily invest in NPP shares, which allows a large number of investors to be involved, mobilises additional capital and gives a market valuation for NPP shares.

The construction of a nuclear power plant in the SaHo Model offers many benefits to the various stakeholders involved in the project:

- government;

- investors;

- energy consumers;

- as well as the climate, which is a silent stakeholder in all zero-carbon energy projects.

For more information on various aspects of the SaHo Model, see our publications and interviews:

![]()